Need to determine your property’s flood risk? Let’s take a look at how to know if your property is in a flood hazard area and ways to remedy it.

Are you in the floodplain?

As a developer and property owner, your revenue model factors in a number of variables related to your property; a significant factor is the cost to insure your development. Many properties are at a distinct risk of flooding during major rainfall events, and, as you may already know, the Federal Emergency Management Agency (FEMA) National Flood Insurance Program (NFIP) delineates which properties have an actuarial risk of experiencing this.

The NFIP Floodplain Insurance Rate Maps (FIRM) are products of this program that are publicly available to any individual interested in seeing the flood risk of their current or prospective property. These maps can get pretty complicated to understand if you aren’t familiar with the hydrologic terminology. So, to put it simply: if your property falls in a zone labeled as a 1% annual exceedance probability zone (Zone AE in most areas) or floodway, then you are within what is referred to as the 100-year floodplain, or the Special Flood Hazard Area (SFHA). Statistically speaking, this is the area that will presumably flood during a rainfall event that has a 1% chance of happening throughout a given year.

I’m in the floodplain, how do I get out of it?

So your property is partially or entirely within the floodplain, and you are on the hook for additional flood insurance — and there’s no way to avoid it, right? Not necessarily.

Hydrology is not a perfect science and FEMA recognizes that there are ways to mitigate your risk or demonstrate that your property is mistakenly classified. So they have created a petition process to modify the FIRM map to remove your property from the floodplain. This is done by securing a Letter of Map Change (LOMC).

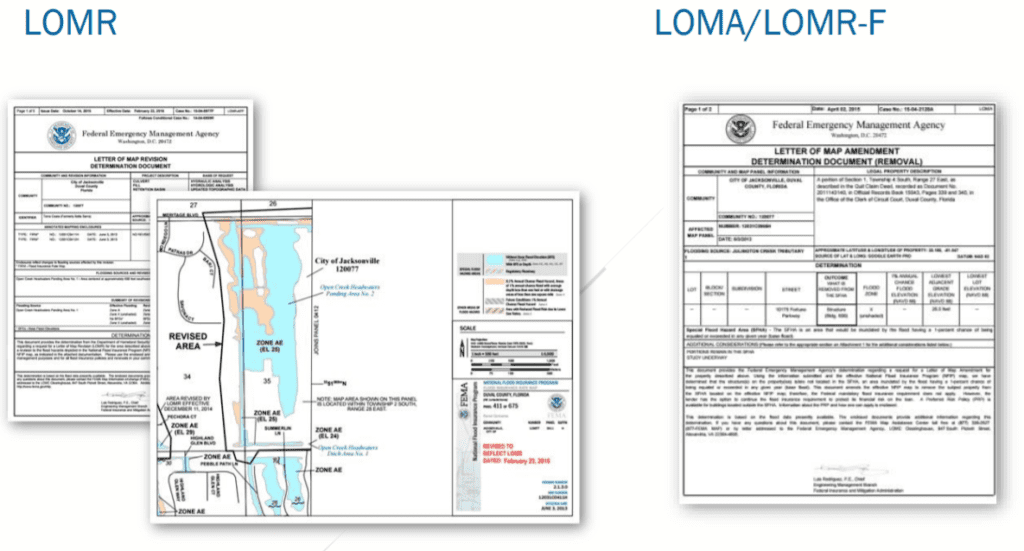

What are the types of Letters of Map Change?

Depending on your development, there are two main options to securing a LOMC which vary with the design of your structure. Here are the basic types of LOMCs applicable to property owners:

- Letter of Map Adjustment (LOMA) – A LOMA is a letter from FEMA stating that an existing structure or parcel of land – that is on naturally high ground and has not been elevated by fill – would not be inundated by the base flood.

- Letter of Map Revision – Based on Fill & Conditional Letter of Map Revision – Based on Fill (LOMR-F & CLOMR-F) – Owners of structures (or parcels of land) raised above the base flood by the placement of fill may request a LOMR-F. Fill is defined as material from any source placed to raise the ground (natural grade) to or above the Base Flood Elevation (BFE).

- Letter of Map Revision & Conditional Letter of Map Revision (LOMR / CLOMR) – This process is generally reserved for municipalities and community developers who are building regional drainage facilities that alter the floodplain and floodway directly. The technical requirements are much greater and can require a lengthy review process from FEMA and local agencies.

How do you apply for a Letter of Map Change?

FEMA has standardized application procedures that every property follows. Of primary importance, each type of map change will require the applicant to produce an Elevation Certificate signed and sealed by a Professional Land Surveyor. This document demonstrates that the structure is sufficiently above the floodplain according to local floodplain regulations. If a “conditional” change is requested, then a professional engineer or surveyor must demonstrate that the proposed conditions will also raise the property out of the floodplain and meet local floodplain criteria. It is generally recommended that a professional engineering consultant guide you through this process.

A LOMC can take anywhere from two to six months for final approval from FEMA, so it is important to start the process as soon as possible during your development. Once the letter is secured, you can provide it to your insurance company to reduce or eliminate the flood insurance requirement for your property.